LET’S TALK ABOUT HOW DENTAL INSURANCE PLANS REALLY WORK!

We need to talk about dental insurance. Very few people fully understand how dental insurance plans work. The biggest pill to swallow is that every dental insurance policy differs. To help, we’ll discuss some terms that conform across most plans. However, each policy retain the right to include a different definition, which can make a world of difference as to how the plan actually operates.

We need to talk about dental insurance. Very few people fully understand how dental insurance plans work. The biggest pill to swallow is that every dental insurance policy differs. To help, we’ll discuss some terms that conform across most plans. However, each policy retain the right to include a different definition, which can make a world of difference as to how the plan actually operates.

DENTAL INSURANCE PLANS: TERMINOLOGY

WAITING PERIOD

Just because you’re paying for dental insurance does that mean you have coverage? If you’re paying for dental insurance you at least have some coverage but all the benefits may not  immediately kick in because there may be a waiting period.

immediately kick in because there may be a waiting period.

The insurance company wants to retain your business but if you’re new to the plan it may withhold some benefits as they don’t want to pay for everything right away and then you leave the plan because you received what work you wanted or needed. The waiting period entices you to stay and each year the benefits get richer. In the beginning they won’t pay for implants; a couple of years later it becomes a richer benefit plan so they’ll put some money towards implants. Waiting periods range from 6 to 12 months before any standard work can be done. Waiting periods for major work are typically longer and can be up to two years. These periods are set in place by insurance companies to guarantee they’ll profit off a new account and to discourage people from applying for a new policy to cover impending procedures.

DEDUCTIBLES, CO-PAYS AND CO-INSURANCE

An insurance deductible is the minimum that must be paid before the insurance policy pays for anything. For example if the deductible is $200 and the covered individual’s procedure is $178, the insurance does not kick in, and the individual pays the entire amount. Co-pays, which are a set dollar amount, may also be required at the time of the procedure.

If a deductible is met, most policies only cover a percentage of the remaining costs. The remaining balance of the bill paid by the patient is called co-insurance, which typically ranges from 20 to 80% of the total bill.

HOW DENTAL INSURANCE CATEGORIZES AND PAYS FOR PROCEDURES

Dental procedures covered by insurance policies are typically grouped into three categories of coverage: preventative, basic and major. Most dental plans cover 100% of preventative care such as annual or semi-annual office visits for cleaning, X-rays and sealants. The coverage for the exam can vary as well. Dentists normally do 3 different types of exams, the comprehensive, the limited exam and the periodic exam.

The comprehensive exam is exactly like it sounds, this is the ideal examination, for it is the most extensive dental examination. The dentist will perform a comprehensive hard and soft tissue examination that includes: oral cancer screening examination; mouth- mirror, explorer, and periodontal probe examination; adequate natural or artificial illumination; panographic or full-mouth, pericapical, and posterior bitewing radiographs; blood pressure recording; and when indicated, percussive, thermal and electrical test. Included are those lengthy clinical evaluations required to establish a complex clinical diagnosis and the formulation of a total treatment plan. For example: treatment planning for full-mouth reconstruction; determination of the etiology or differential diagnosis of a patient’s chief complaint, such as temporomandibular joint (TMJ) dysfunction and associated oral facial pain; or lengthy history taking relative to determining a diagnosis. Comprehensive, right? The number of comprehensive exams is limited to one every 3 years in many cases.

The limited exam is also how it sounds. The limited exam concentrates on a specific problem and the exam just concentrates on the specific problem the patient is having. There are many insurance companies that will not pay for the limited exam.

The periodic exam is a benchmark examination. Your first exam is the comprehensive, your next teeth cleaning will be a periodic exam and the periodic exam is then done on each hygiene appointment. As your teeth have been initially charted the benchmark serves to record any changes as a benchmark. This is usually paid with your cleaning.

Basic procedures are treatment for gum disease, extractions, fillings, and root canals, with deductibles, co-pays and coinsurance determining the patient’s our-of-pocket expenses. Most insurance policies cover 70 to 80% of these procedures, with patients paying the remainder.

Major procedures such as crown, bridges, inlays and dentures are typically only covered at a high-copayment, with the patient paying more out-of-pocket expenses than other procedures. Every policy differs in how procedures are categorized as preventative, basic and major, so it is important to understand what is covered when comparing policies. Percentage of coverage can also fluctuate to a large degree. Some policies group root canals as major procedures, while others treat them as basic procedures and cover much more of the cost.

DENTAL INSURANCE DOES NOT COVER COSMETIC PROCEDURES

Most dental insurance policies do not cover any costs for cosmetic procedures, such as teeth whitening, tooth shaping, veneers and gum contouring. Because these procedures are intended to simply improve the look of your teeth, they are not considered medically necessary and must be paid for entirely by the patient. Some policies cover braces but usually require paying for a special rider and/or delaying braces until after a lengthy waiting period.

YEARLY MAXIMUM

While most medical insurance policies have yearly out-of-pocket maximums, the majority of dental policies cap the amount of annual coverage. Coverage maximums typically range from $750 to $2,000 per year and generally speaking, the higher the monthly premium, the higher the yearly maximum. Once the yearly maximum is reached, patients much pay for 100% of any remaining dental procedures.

So that’s the basic definitions in use today. Most people associate the word insurance with the concept of protection. We buy insurance to safeguard ourselves against unforeseen, large expenses. Dental Insurance is not designed to pool risk or to protect anyone from unforeseen expenses, which is traditionally what insurance is designed to do. What we call dental insurance most often functions more like a discount coupon than a form of insurance. In fact, it’s simply a way for employers to help their employees offset some of the cost of dental care. It is not designed to pool risk or to protect anyone from unforeseen expenses which is traditionally what insurance is designed to do. Because of this relative predictability, most dental insurance companies know what their claims experience will be and can sell plans to employers accordingly.

GET THE MOST OUT OF YOUR DENTAL INSURANCE

So here are some things you can do to get the most out of your coverage:

- Make sure you understand your plan fully, particularly its restrictions. If you have questions, talk to your company’s human resources person or call the insurance company’s toll-free number.

- Let your dentist’s office help you get the most out of your coverage. While dental insurance plans can be confusing, this is a world (complete with its own language) in which your dentist’s staff functions every day, and most are willing to help you figure it out. They might even be able to help you get an allowance towards the cost of a procedure that’s not explicitly covered (for example, put the money you would have gotten for a bridge towards an implant instead). But remember, it’s your insurance, and while your dental office can help you interpret the language, you are your best advocate in getting the benefits to which you are entitled, and that are specified in your policy. They may not know every policy, in fact, they don’t as every plan is different, but they do know how to get to the meat of the policy and can provide usually a good estimate of the cost of care for you.

- Work out with your dentist how to pay for what’s not covered. Many offer options to spread payments over time. Neglecting care will cost you more money in the long run. A lot of money. You may be able to make a separate financial arrangement with your dentist for the care you need, and have your insurance company reimburse you directly to the extent that the procedures you need are covered. This may work out better for you and your dentist.

Do remember that that your treatment plan presents an estimate of the cost of the treatment. Insurance companies can downgrade a procedure after the claim is presented to them and therefore end up costing more than the treatment plan said. Other things such as deductibles or co-payments, co-insurance, wait times and missing tooth clauses can also change the formulas.

Finally, keep in mind that at the end of the day you are in charge of your own healthcare — not your employer, your insurance company, or even your dentist. Don’t let a lack of coverage keep you out of the dentist’s chair for inexpensive routine maintenance. If you don’t have insurance at all, it’s even more important to make that minimal investment in your health and the health of your children by going twice yearly. That’s really the best dental insurance anyone can buy.

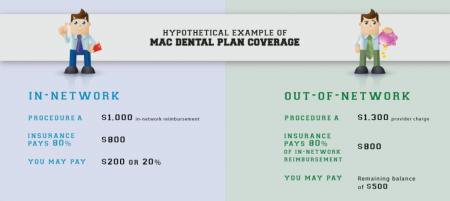

IN-NETWORK

Many people mistakenly believe when they go to their dentist who is contracted (or in network) with an insurance company, (say Delta Dental), the dentist represents the insurance company. Not True. Your dentist receives a fee schedule, the insurance company’s fee schedule, at the time they contract. This gives the dentist a right to be advertised on the insurance company’s list of in network providers. Being “In Network” dictates the maximum fee the dentist may charge for treatment procedures allowed by the insurance company. (For example: The regular fee for a crown is $1000 but the insurance contracted fee is $800.00 and they pay 50% of that. The dentist then cannot charge more than the contracted fee for allowed procedures.)

Your dentist has NO relationship beyond this agreement with your insurance company! And remember (technically), no dentist is obligated to determine benefit allowances, bill your insurance, or deal with the problems that may come up to collect from the insurance company…In network or not! Except for the fact they want to get paid for services provided. Dealing with insurance is very time consuming and expensive for a dental clinic. It requires hiring full time insurance billing staff to ensure navigating through the complications and requirements involved with filing claims to collect from the insurance companies.

Insurance billing service has kind of evolved into a “required service” due to the language, code submission complications and other details the patient is not in a position to understand or deal with in many cases. For these reasons, insurance billing services are not optional for a majority of clinics. Clinics simply must offer this service unless they only do business on a cash basis, not too realistic in today’s world. But it is a service provided that is often misunderstood.

HOW TYPICAL DENTAL INSURANCE PLANS OPERATE

So you have insurance, and you go to the dentist; here is generally how it will work:

- Your dentist office will call your insurance at the time of service, or before, to verify eligibility, and for “ESTIMATED” benefit allowances for different procedures under your plan. I emphasize “estimated” as ALL insurance companies include a disclaimer by phone or online which state that all benefit percentages provided are “not a guarantee” and are only “estimates of coverage payment”. (I’ll get to why shortly.)

- Your dentist will present to you, hopefully in advance of treatment, what the total fee is for the procedure you need, and what “estimated” percent your benefit plan pays of that procedure. The balance remaining is the Co-Pay or out of pocket expense to you. Most plans also require a deductible charge that must be collected at the time of service.

- Your dentist performs the procedure, you pay your deductible and co-pay, the clinic bills the insurance company for the benefit allowance, and everyone is happy right?

Not so fast. The devil is in the details as they say. Here are just a few details that often put the dental clinic in an undesirable position. These details are why dealing with insurance companies can be: expensive, patient relationship damaging, and generally a pain in the back side for dentists. So let’s talk “Codes”, “Estimates”, and “Billing”.

Your dentist determines “Clinic fees” he or she will charge for various treatment procedures (known in the profession as “Usual and Customary Fees”), according to a list of fees that are usual and customary for your area, according to the zip code of the clinic location. These fees are recommendations that range from a low end fee, mid range fee, or high end fee for a particular procedure. The particular fee your dentist may select depends on lots of factors, generally related to the overall cost of business. All dental treatment procedures are assigned a “code number” that all dentists use. These codes are universal and every dentist must use them to define the treatment procedure and corresponding charge for billing.

INSURANCE

Insurance companies use these same codes in billing. However, they establish what dollar amount or percent will be assigned a particular procedure code for an individual plan benefit. They also limit the Maximum fee (as mentioned above) the dentist may charge for codes/procedures covered by an individual plan. Not all codes or procedures are automatically covered. Insurance company benefits under your plan (what codes are covered and what percent of the fee is covered) vary according to the plan benefits established by your particular plan.

What codes are covered can often have “conditions” attached to them that allow for denial of payment for all or part of what you (and the dentist) think is covered, based on what information is provided at the time they call for eligibility and benefits for your plan.

For example: Joe patient goes to a great Emergency Dental Care clinic that provides same day care on a Saturday because his tooth is throbbing and nothing helps. His regular dentist is closed until Monday. The emergency clinic dentist also is in network with his dental insurance carrier, so Joe is not concerned. Joe decides to get the work done, makes his co-pay, and does the treatment. A few months later, Joe gets a bill from the clinic for the full cost of the exam and x-ray! Why?

Turns out under his individual plan, there is an exclusion or condition for “Emergency Care” which says the treatment procedure cannot be performed on the same day the Exam and X-ray is done! Benefit denied. Joe did not know this, and when the dentist’s staff called in to determine eligibility and benefits, they can’t learn of these disqualifying conditions either. It’s extremely frustrating for patients and the dental clinic alike.

As another example, the dentist does not know the patient he just helped used up the plan annual allowance for “preventive” care exam and x-rays, two days before at another clinic. This fact was not available at the time of billing and payment ends up denied. So the dentist ends up sending out bills and often is left unable to collect for service provided.

SO MANY SCENARIOS, SO MANY PLANS, THE MAGIC TRIANGLE

These are just two examples of many that could be given, of issues that come up dealing with insurance for patients. That is why most dentists, when presenting the cost for treatment to patients using insurance, make sure they sign for the fact they are ultimately responsible for the total amount of service fees. Eligibility and Benefit allowances are all the dentist can determine up front! The fine print exclusions, only the insurance company is privy to, are the reason dentists and the patient only get “Estimates” of coverage at the time of service.

Here is another common insurance problem. Let’s say a patient has a refund coming for fees charged by the clinic at the time of service (because the clinic is not sure the insurance will fully cover a portion of the treatment). A week, a month goes by and no refund has arrived from the dental clinic. The patient calls the dentist’s insurance clerk and is told no check has been received from the insurance yet! Upset, they call their insurance company who tells them, “yes!” that check was processed and was issued to the provider. So they call back the dental clinic convinced someone is lying and earning interest off money received but not refunded.

It’s not that the insurance company representative lied, or that the dental clinic did, its often what the insurance company representative does not tell the customer that is the problem. (You see they don’t want to be the bad guys, it’s just prudent for them to let the dentist take the heat.) The claim may have been received, a check issued, and they may even provide a date when it was done! But all of those true facts may not mean the check was actually approved and mailed!

Standard procedure may be to approve issuing a check, but the next standard procedure may be to have the claim reviewed by in-house dental review experts to determine if the claim is clinically legitimate. Or, they may request additional information or x-rays from the clinic, before the payment is actually approved to send out. Whatever; sometimes receiving payment just takes forever and you (and the clinic) can never figure out why?

If you have been around very long you have learned insurance carriers expect prompt premium payment, but often exercise the right to delay benefit payments until every (t) is crossed and every (i) dotted of their own making.

When something like this happens to a patient, and they are under the misguided belief the dentist is in cahoots with the insurance company, or is being dishonest, who do you think they call first to vent their anger? Most often the dental clinic!

Yes, just like in all industries there are more trustworthy players than others. That’s true for insurance carriers and dentistry as well. If you have dental insurance it is a blessing to help you afford dental care. Most dental offices want to help you get the maximum benefit allowed under your plan.

Hopefully this article gives the reader a tiny glimpse into the complications in dentistry of managing claims for a host of individual plans through multiple insurance providers. But I trust folks at least take away an understanding that dentists are NOT partners with or in collusion with, Insurance Companies.

So who should you trust? That’s for you to use your best judgment about. But remember, unlike the people making decisions about claims and cutting checks for some huge far away insurance company, your dental care provider is local and accessible to meet in person. Should you become dissatisfied or encounter a problem along the way, remember the dental office person who is handling insurance claims for you, usually has no reason not to help you understand and resolve insurance issues (unless you give them one). They are usually more than willing to work with you, as the dentist can’t get paid either unless insurance payment issues are resolved.

I call this the magic triangle PATIENT — INSURANCE Company — PROVIDER (dentist) because when it really works right, it’s like magic and you blink your eyes twice and go WOW. Many times though it’s more like one corner is pitted against another. But if everyone has a good basic understanding then it is really easier to work it out and have a little patience.

The bottom line to this whole discussion is to talk of THE END OF THE YEAR. You’ve paid all year on your insurance premium for a set of benefits. With most insurance companies the benefits do not carry over to the New Year. You want to make sure you’ve used all of your yearly spend in your plan. If you’ve used $1200 and you have an annual maximum of $1500 there is still $300 left in your plan and if you don’t use it, the insurance company then pockets that $300. Every time you get your teeth cleaned although there is no charge to you out of pocket, the cost goes against your yearly maximum. Take care of your teeth throughout the year as there will be far less cost to you in the end for maintaining your teeth.

Go Back